What Is Hyperliquid DEX, and Why Has It Become So Popular?

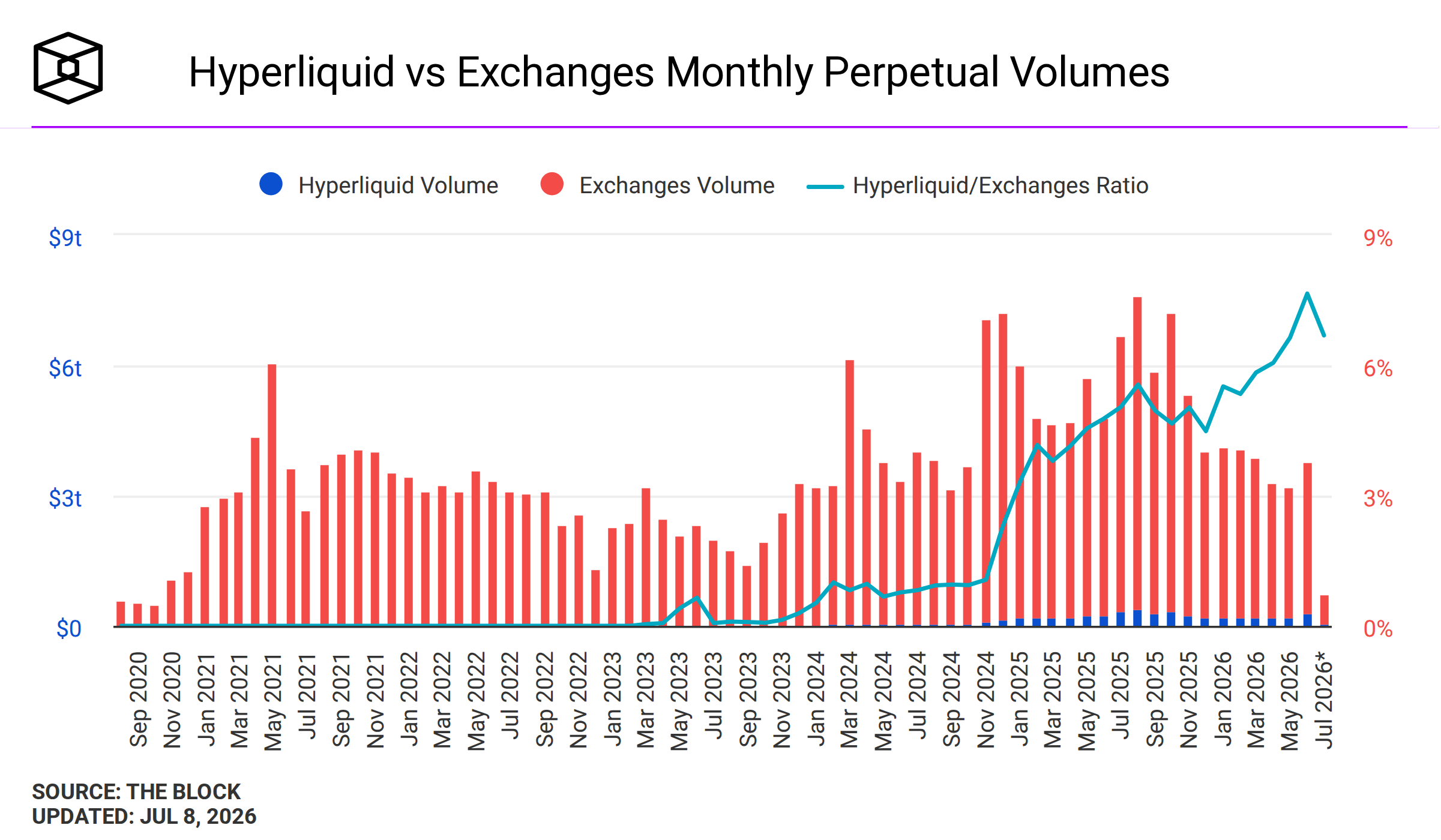

Hyperliquid is a decentralized exchange (DEX) for perpetual futures, built on its own purpose-made blockchain. It lets traders open long and short positions on crypto, and increasingly on stocks and commodities, without a custodian holding their funds. Launched in 2023, it now handles roughly 40% of all on-chain perpetuals volume, with over $250B in monthly trading.

What Are Perpetual Futures?

Before getting into what makes Hyperliquid different, it helps to be clear on what it actually sells: perpetual futures, usually shortened to "perps."

A regular futures contract has an expiry date. You agree today on a price for some future delivery date, and when that date arrives, the contract settles. A perpetual futures contract removes the expiry date entirely. You can hold a position for a day or for years, as long as you keep enough collateral to support it. To keep the contract's price tracking the actual market price without an expiry to force convergence, perps use a mechanism called the funding rate: periodically, longs pay shorts or shorts pay longs, depending on which side of the trade is crowded. That small, recurring payment is what tethers the perpetual contract's price to the underlying asset.

The idea of a derivative contract without a fixed expiry isn't new. Economist Robert Shiller proposed a similar structure for equity index exposure back in 1993. What was missing for decades was a market willing and able to run it at scale. Crypto exchange BitMEX is generally credited with making perpetual futures work in practice, launching a Bitcoin perpetual swap in 2016 that became one of the most heavily traded derivatives in crypto. Since then, perps have become the dominant way traders take leveraged, directional positions in crypto, generally trading far more volume than traditional dated futures on the same assets.

A quick example makes the funding rate concrete. If more traders are long Bitcoin perps than short, the funding rate typically turns positive, and longs pay shorts a small percentage of their position size, often every hour or every eight hours depending on the venue. That payment makes holding the crowded side of the trade slightly more expensive over time, which pulls the perpetual's price back toward the spot price and discourages one-sided positioning from running unchecked. It is a small, mechanical detail, but it is the entire reason a contract with no expiry date doesn't just drift away from reality.

This matters for understanding Hyperliquid specifically, because the exchange's speed and design choices (discussed below) largely exist to make this funding mechanism, and the liquidations that follow when a trader's collateral runs out, work reliably under load. A perpetuals exchange that can't process funding payments and liquidations quickly during a volatile move isn't really competing on the same terms as one that can.

It's also worth being precise about what "on-chain" adds here. A centralized exchange like Binance or Coinbase runs the same basic mechanism, funding rates and liquidations, but inside a private, off-chain matching engine. The trader has to trust that the exchange is calculating and enforcing this correctly and holding their collateral safely. An on-chain venue like Hyperliquid settles the same mechanism through public, verifiable transactions, and the trader's collateral sits in a wallet they control rather than in the exchange's balance sheet.

Perpetual futures replace a fixed expiry with a periodic funding payment between longs and shorts.

What Is Hyperliquid, Specifically?

Hyperliquid is a decentralized exchange built specifically to trade perpetual futures on-chain. A few things separate it from a typical DeFi protocol:

It has its own Layer 1 blockchain. Rather than deploying as a smart contract on an existing chain like Ethereum or Solana, Hyperliquid built its own purpose-made blockchain (launched in 2023) with trading performance as the design priority. This is closer to how a traditional exchange's matching engine is built for speed, except the ledger is public and on-chain instead of sitting inside a company's private infrastructure.

It uses an order book, not a liquidity pool. Many earlier on-chain derivatives platforms, such as GMX and Synthetix, used a pooled liquidity model, where traders effectively take the other side of a shared vault. Hyperliquid instead runs a central limit order book, the same structure used by centralized exchanges like Binance or Coinbase, matching individual buy and sell orders directly. This tends to produce tighter spreads and more familiar order types for traders coming from centralized platforms.

It is non-custodial. Users connect a wallet and deposit collateral under their own on-chain account. Hyperliquid the protocol never takes custody of user funds the way a centralized exchange does when you deposit into an exchange-controlled wallet.

Concretely, this changes who can lose your funds and how. On a centralized exchange, your balance is an entry in that exchange's internal database, and you are trusting the exchange's solvency, internal controls, and willingness to honor withdrawals. FTX is the reference case for what happens when that trust is misplaced. On Hyperliquid, the collateral backing your positions sits in an account you control; the protocol can facilitate trades and enforce liquidations against it according to its rules, but it isn't holding a pool of customer funds that could be commingled or misused the way a centralized custodian's balance sheet can be. That doesn't eliminate risk; it changes its shape, shifting the questions toward smart contract correctness, oracle reliability, and validator behavior rather than counterparty solvency.

Hyperliquid was founded by Jeff Yan, who previously ran the high-frequency trading firm Chameleon Trading, and launched in early 2023. Its timing was notable: it arrived a few months after the collapse of FTX, at a moment when a large part of the crypto trading community was actively looking for alternatives to trusting a centralized exchange with custody of their funds.

Hyperliquid is easier to place next to the on-chain perp platforms that came before it, since the differences explain a lot of what follows.

| Platform | Liquidity model | Where it runs | Trader experience |

|---|---|---|---|

| GMX, Synthetix | Pooled vault (traders take the other side of a shared pool) | Smart contracts on an existing chain | Simple, but spreads and slippage depend on pool size |

| dYdX (early versions) | Off-chain order book, on-chain settlement | Layer 2 on Ethereum, later its own Cosmos chain | Order book feel, but not fully on-chain matching |

| Hyperliquid | On-chain central limit order book | Its own purpose-built Layer 1 | Closest to a centralized exchange, fully on-chain |

Why Did Hyperliquid Grow So Fast?

On-chain perpetual exchanges existed well before Hyperliquid. dYdX, GMX, and Synthetix all had meaningful volume. What Hyperliquid did differently was solve two problems that had held the category back: liquidity and speed.

It bootstrapped its own liquidity. New exchanges usually need professional market makers to provide tight spreads, which is expensive and slow to arrange. Hyperliquid instead built HLP, the Hyperliquidity Provider vault, a market-making strategy run by the protocol itself that any user can deposit into. Depositors share in the vault's trading profits (and losses), and in exchange the exchange gets liquidity from day one without needing to strike deals with external trading firms first.

This is a different way of solving the classic chicken-and-egg problem every new exchange faces: traders won't come without tight spreads and deep order books, and market makers won't provide those without enough trading volume to make it worthwhile. By socializing the market-making function itself, rather than paying a small number of professional firms to provide it, Hyperliquid effectively turned its own userbase into its initial liquidity provider, funded by anyone willing to accept the vault's risk profile in exchange for a share of its returns.

It matched centralized-exchange speed and user experience. The recurring complaint about earlier on-chain perp platforms was that they felt slow and clunky compared to a centralized exchange's app: laggy order execution, limited order types, or origination on a general-purpose chain not optimized for trading. Because Hyperliquid built its own chain for this exact purpose, order execution and interface responsiveness are much closer to what traders already expect from centralized platforms.

The result shows up in the market share numbers. On-chain perpetual trading went from under 1% of total (centralized plus decentralized) perp volume in early 2023 to roughly 14% by mid-2026, and Hyperliquid alone now accounts for something close to 40% of all on-chain perp volume, with monthly trading volume regularly exceeding $200B.

Distribution also played a role. Rather than selling tokens to venture funds ahead of launch, Hyperliquid allocated a large share of its HYPE token supply to past users of the platform, based on trading activity accumulated before the token existed. Whatever one thinks of that as a token design choice, the practical effect was to give early users of the exchange, rather than only its investors, a direct stake in its growth, which reinforced the same loop: more traders, more volume, more depth in the order book, better execution for the next trader in line.

How Trades Actually Get Matched and Liquidated

The phrase "on-chain order book" deserves a moment, since it is the detail that makes Hyperliquid's speed claims credible rather than marketing.

On a typical smart contract chain, every order, cancellation, and match would need to be its own on-chain transaction, competing for block space and paying gas, which is far too slow and expensive for active trading. Hyperliquid's own Layer 1 is built around a custom consensus mechanism designed to process this volume of order flow directly, with the order book itself living as a core part of the chain instead of an application bolted on top of a general-purpose one. That's the practical reason Hyperliquid can offer sub-second order matching at a cost structure competitive with centralized exchanges, something earlier smart-contract-based perp DEXs generally could not do without moving order matching off-chain first.

Liquidations work on a similar principle. When a trader's collateral falls below the maintenance margin required to support their position, given how much leverage they're using, the protocol needs to close that position quickly, before losses exceed the collateral backing it. On a slow chain, a backlog of liquidations during a fast market move can leave the protocol holding bad debt. Hyperliquid's HLP vault plays a role here too, acting as a backstop liquidity provider that can absorb positions being liquidated when there isn't enough external counter-liquidity in the order book at that exact moment.

HyperEVM and the Wider Ecosystem

Hyperliquid isn't only a trading venue anymore. Alongside its core exchange (often called HyperCore), the protocol runs HyperEVM, an Ethereum-compatible smart contract environment that sits on the same chain and can read and interact with the order book and its liquidity directly.

That has seeded a small but growing ecosystem of third-party applications built on top of Hyperliquid's liquidity rather than around it: lending protocols that use Hyperliquid positions as collateral, structured products built on the vault system, and interfaces that offer a different front end to the same underlying order book. It is a different growth pattern than a single exchange trying to build every feature itself, and it means some of Hyperliquid's usage and volume figures now include activity from applications a trader might not directly associate with the Hyperliquid brand, something to keep in mind when comparing headline numbers across platforms.

Beyond Crypto: Permissionless Markets

Hyperliquid's more recent expansion runs through a feature called HIP-3, which allows any qualified third party to list a new perpetual market on the protocol and earn a share of the fees it generates, without needing Hyperliquid itself to build and list the market first.

In practice, this has extended to perpetual markets on assets well outside crypto: commodities such as gold, silver, and oil, and even pre-IPO or private company valuations. One useful way to think about it: traditional futures exchanges are closed on weekends and holidays, while an on-chain, always-running order book is not. That difference matters most exactly when it is hardest to trade elsewhere, when a market-moving weekend headline lands and the traditional futures market for that asset is closed, but an on-chain market for it stays open.

Mechanically, HIP-3 works a bit like an app store for markets. A deployer stakes a bond in HYPE, defines a new market (the underlying asset, its oracle price feed, margin requirements), and the market goes live for anyone on Hyperliquid to trade, with the deployer earning a cut of the fees it generates. This is a meaningfully different model from a traditional exchange, where a listings committee decides what gets added, or from earlier DeFi protocols, where adding a new market usually required a governance vote and a code change.

The bond requirement is the mechanism that keeps this from becoming a free-for-all. Because a deployer has capital at stake, and because a badly designed market (a manipulable price oracle, for instance) can be exploited at the deployer's expense, there's a built-in incentive to design new markets carefully instead of listing anything possible purely to capture fees. It's a market-based alternative to a centralized listings committee, with its own tradeoffs: faster and more permissionless, but reliant on the bond size and the community's diligence rather than a single gatekeeper's review.

This is worth understanding as a structural trend, not as a specific trading recommendation. The instruments themselves (equities, commodities, novel private-market tokens) carry different risk profiles and, in some cases, an unresolved regulatory status.

What Is the HYPE Token?

Hyperliquid has a native token, HYPE. A portion of the protocol's revenue is used to fund an ongoing buyback of the token from the open market, a capital allocation approach that mirrors how some public companies use free cash flow to repurchase shares.

The mechanism itself is straightforward to describe: trading fees and other protocol revenue accumulate, and a defined share of that revenue is used to buy HYPE on the open market on an ongoing basis, instead of being routed to a separate treasury or team allocation. That's a factual description of how the token's economics are structured, and it's the extent of what belongs in a fundamentals piece. It says nothing about whether the token is well valued at any given price, what its trading volume or volatility looks like, or how its supply schedule compares to other protocol tokens, all of which would be required for any actual investment analysis.

That is the extent of what belongs in a fundamentals explainer. This article is not the place for a view on HYPE as an investment, and Stoic AI does not offer HYPE, or any other token, as an investment product. If you come across content elsewhere making a price or return case for HYPE, treat it as a separate category of claim from anything about how the exchange itself functions.

What to Know Before Using Hyperliquid

Non-custodial and permissionless are real advantages, but they come with tradeoffs worth being explicit about.

No KYC, and no safety net that comes with it. You don't need to submit identity documents to trade. That also means there's no centralized support team to call if you lose access to a wallet or send funds to the wrong address. Self-custody puts the operational responsibility on the trader.

Geofencing and an unsettled regulatory picture. Hyperliquid geofences US persons, and the regulatory treatment of crypto perpetual futures in the United States has been in motion. As of mid-2026, the CFTC has taken steps toward allowing regulated crypto perpetual futures under existing futures rules, a shift from the near-total absence of onshore US perp products in prior years. This is a live, evolving area rather than a settled one, and anything written about it today may look different in a year.

For context on why this shift is happening now: the absence of onshore US perpetual futures for most of the last decade was, by most accounts, less a considered policy decision than a byproduct of which products incumbent US exchanges chose to list under existing futures rules. Recent CFTC actions, including clearing a path for a US-listed bitcoin-referenced perpetual and allowing a major exchange to offer certain crypto perpetuals through a foreign affiliate treated as foreign futures, suggest regulators are now working within existing frameworks rather than waiting on new rulemaking. None of this changes Hyperliquid's own status today, which remains an offshore, geofenced venue, but it is part of why the broader perps category is getting more attention from traditional finance.

API key security matters more, not less. Because there's no custodian to fall back on, the security of whatever keys or wallet access you grant to any tool, including a trading bot, is the main thing standing between your funds and a mistake or exploit.

Smart contract and oracle risk replace some custodial risk; they don't cancel it out. Removing a centralized custodian from the equation doesn't mean removing risk from the equation. Hyperliquid's chain, its liquidation engine, and the price oracles feeding its markets are all software, and software has bugs. A protocol exploit or an oracle malfunction during a volatile market can produce losses in ways that look different from a custodian collapse but aren't necessarily smaller. Anyone moving from a centralized exchange to Hyperliquid is trading one category of risk for another, not trading risk for safety.

How Stoic AI Fits In

Stoic AI's Meta strategy, a market-neutral system that trades across more than 40 crypto perpetuals at once, now runs on Hyperliquid in a fully non-custodial setup. The strategy executes trades on the trader's own Hyperliquid account through trade-only permissions; it can open and close positions, but it cannot withdraw funds, and the connection can be revoked at any time.

This matters specifically because it addresses a real gap the fundamentals above point to. A systematic strategy trading 40-plus perpetuals around the clock needs an execution venue that can actually keep up, both in terms of raw speed and in terms of not requiring the user to hand over custody just to get access to that execution. Hyperliquid's order book model and non-custodial architecture line up with those two requirements more directly than a pooled-liquidity DEX or a centralized exchange deposit would.

"Running Meta on Hyperliquid was a natural next step, not a pivot. The strategy doesn't change based on where it's executing, but the setup does: the user keeps custody of their funds the entire time, and we simply plug the strategy in as a trade-only connection. That removes an entire category of counterparty risk from the equation, which matters a lot more to institutional-minded users than a marginal fee difference does."

Nodari Kolmakhidze, CFO and Partner, Stoic AI

If you want the specifics of how the Meta strategy is structured and how the Hyperliquid connection works, the Hyperliquid trading bot page and the Meta strategy page go into more detail, including the current fact sheet.

Who Hyperliquid Tends to Suit

Hyperliquid isn't a fit for every trader. It tends to suit people who already trade perpetuals elsewhere and want tighter execution or lower counterparty exposure, developers and funds building automated strategies who value an open, verifiable order book, and traders comfortable managing their own wallet security without a support desk to fall back on.

It tends to suit fewer people who want a simple, custodial, app-store-style experience with account recovery and customer support, who are trading small, infrequent amounts where the gas and setup overhead of a wallet isn't worth it, or who are located somewhere the platform geofences.

None of that is a verdict on Hyperliquid as a platform. It's a reasonably common pattern across non-custodial, on-chain products generally: the tradeoffs that make them attractive to one type of user are the same tradeoffs that make them a worse fit for another.

The same pattern shows up when comparing Hyperliquid to specific centralized exchanges rather than to the category in the abstract, since Binance and Coinbase, for example, sit at different points on this spectrum themselves. We cover the Coinbase side in depth in Hyperliquid vs Coinbase: Which Should You Trade On?, since the right answer depends heavily on what a given trader already values: familiarity and fiat on-ramps, breadth of listed assets, or the non-custodial structure this article has focused on.

FAQ

What is Hyperliquid used for?

Hyperliquid is used to trade perpetual futures, contracts that let traders go long or short on an asset's price without an expiry date, without a centralized custodian holding their funds. It supports crypto perpetuals and, through HIP-3, markets on other assets such as commodities and equities.

How does Hyperliquid work?

Hyperliquid runs on its own purpose-built Layer 1 blockchain and matches trades through an on-chain central limit order book, similar in structure to a centralized exchange but settled on-chain. Traders connect a wallet, deposit collateral, and open positions directly, without handing custody of funds to the platform.

Is Hyperliquid safe?

Hyperliquid is non-custodial, which removes one category of risk (a custodian misusing or losing funds). It does not remove other risks, including smart contract risk, self-custody responsibility, and the general volatility of leveraged trading.

Is Hyperliquid regulated?

Hyperliquid operates outside the US regulatory perimeter and geofences US persons. The regulatory treatment of crypto perpetual futures in the US has been changing, with the CFTC taking steps in 2026 to open a path for regulated crypto perps under existing futures rules, but this remains an evolving area.

What is the HYPE token?

HYPE is Hyperliquid's native token. A share of the protocol's revenue is used to fund an ongoing token buyback. This is background information about how the protocol is structured, not investment guidance, and Stoic AI does not offer HYPE as an investment product.

Why is Hyperliquid so popular?

Hyperliquid grew quickly by bootstrapping its own liquidity through a public market-making vault, matching the speed and user experience of centralized exchanges, and later expanding into new market types through permissionless listings. It now accounts for a large share of all on-chain perpetuals trading volume.

Is Hyperliquid a centralized or decentralized exchange?

Hyperliquid is decentralized. Trades are matched and settled on its own public blockchain, and user funds remain in wallets the user controls, rather than in accounts held by the exchange, which is the defining feature of a centralized exchange.

What is HIP-3?

HIP-3 is the Hyperliquid feature that lets a third party stake a bond and list a new perpetual market, on assets ranging from crypto to commodities to equities, without needing Hyperliquid itself to build and list that market first, earning a share of the fees the new market generates.